Reverse Mortgages

What is a Reverse Mortgage

Definition: A reverse mortgage is a loan to a senior secured by a mortgage lien on the senior's house which she owns and occupies, with most of the loan proceeds usually paid out over time rather than upfront, and with no repayment obligations so long as the senior lives in the house.

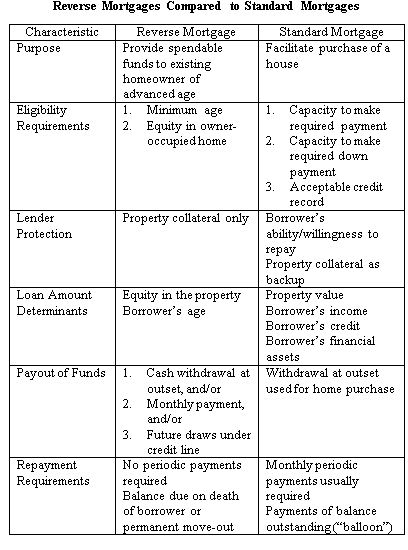

Purpose: A reverse mortgage is designed to provide an elderly homeowner with spendable funds that can be used for a variety of purposes. This is in contrast to a standard mortgage, the major purpose of which is to facilitate the purchase of a house or to refinance a mortgage that has been taken out earlier for that purpose. A summary of the principal features of each is shown in the table.

Eligibility Requirements: To obtain a standard mortgage, borrowers usually must demonstrate that they have sufficient income to make the required payments, that their character is such that they will make every effort to do so, and that their down payment is adequate. In addition, the property that is the collateral for the loan must be in good condition, and marketable.

On a reverse mortgage, there are no income or credit requirements. There must be significant equity in the property. Lenders depend solely on sale of the property after the borrower dies or moves out permanently to be repaid. To be eligible, therefore, reverse mortgage borrowers need only to own and occupy their homes in which they must have significant equity, and to have reached a minimum age.

Lender Protection: On a standard mortgage, lenders look to the borrower to repay the loan, and view the property collateral as their last resort in the event the borrower defaults. On a reverse mortgage, lenders depend wholly on eventual sale of the property to be repaid. The reverse mortgage is expected to terminate before the debt balance grows to exceed the property value.

Loan Amount Determinants: On a standard mortgage, the amount that a home purchaser can borrow depends on the value of the property, and on the borrower’s income, credit and available assets. On a reverse mortgage, the amount a borrower can draw depends on her age and her equity in the home. In both cases, there may be legal and/or regulatory limits imposed on loan amounts.

Payout of Funds: On a standard mortgage, the entire loan amount is disbursed at the outset, as part of a sales transaction or a refinance. On a reverse mortgage, in contrast, the homeowner may receive funds in a variety of ways: as a lump sum at the outset, as a monthly tenure payment which continues until the borrower dies or moves out of the house permanently, as a monthly term payment over a period specified by the owner, or as a credit line of specified amount on which the homeowner can draw at her own discretion.

A particular reverse mortgage program may limit the options to only one or several of these. The oldest program in France was limited to monthly payments until death or move-out, whereas the current Home Equity Conversion Mortgage program in the US offers all the payment options cited above.

Repayment Requirements: Standard mortgages usually require periodic payments that reduce the balance, or at least cover the interest. Most are fully amortizing, meaning that the payments reduce the balance to zero over the term of the loan. Those that are not fully amortizing require that the balance be repaid in full at the end of the term, or after a specified period. Reverse mortgages, in contrast, have no required payments so long as the borrower is alive and occupies the house, but borrowers are free, at least in some programs, to make voluntary payments to reduce their balance.

Debt Changes Over Time: On standard mortgages that require amortization, the debt outstanding gradually declines over time. On those that require only interest payments, the balance is constant until the date when fully amortizing payments begin, at which point the balance begins to decline. Standard mortgages on which the balance rises, referred to as “negative amortization”, are uncommon and disappeared in the US after the financial crisis. On reverse mortgages, in contrast, debt tends to rise over time as interest accrues, since there are no required payments. Borrowers may make voluntary payments to reduce their debt, but this is uncommon.

Borrower’s Rights of

Ownership: Ownership rights are affected only

in that a lien is placed on the property to assure that the borrower meets the

obligations specified in the loan contract. This is the same as with a standard

mortgage, except that with a standard mortgage borrowers have a monthly payment

obligation and on a reverse mortgage they don’t.

Borrower’s Rights of

Ownership: Ownership rights are affected only

in that a lien is placed on the property to assure that the borrower meets the

obligations specified in the loan contract. This is the same as with a standard

mortgage, except that with a standard mortgage borrowers have a monthly payment

obligation and on a reverse mortgage they don’t.Borrower obligations: While there is no loan repayment obligation on a reverse mortgage, the borrower is obliged to pay the property taxes, to keep adequate homeowners insurance in place, and to maintain the property. Failure to comply with these requirements puts them in default, and the lender can institute foreclosure proceedings that would lead eventually to their eviction. A borrower who has someone living with them who is not a party to the reverse contract, such as a spouse, also has a moral obligation to that person. The obligation is to inform that person that they will have to vacate the house if the borrower dies or moves out of the house permanently.

Effects on Borrower Estate: The borrower’s estate receives the equity in the property at the time the borrower dies or moves out permanently. The equity equals the property value net of transaction costs realized through sale, less the balance on the reverse mortgage. Some reverse mortgage options deplete the estate more than others. Cash withdrawals at the beginning will reduce it the most, credit lines that are rarely used will reduce it the least, and monthly payment plans are somewhere in-between. In general, the longer the borrower remains in the house, the larger the depletion of equity.

Title to the House after Borrower Passes: The borrower’s estate can, in general, obtain the title to the house by paying of the reverse mortgage debt. If the value of the house exceeds the debt balance, no problem arises. But if the debt balance is more than the house is worth, the estate has to decide whether or not they want to incur the deficiency.

Fixed Rate or Adjustable Rate: Reverse mortgages can in principle be either. However, reverse mortgages used to secure monthly payments, and/or to reserve a credit line for possible future use, are typically adjustable rate. In the US fixed-rate reverse mortgages are generally available only when the borrower elects to draw all of the proceeds at the outset, with none of it reserved for possible future use.

Upfront costs: These differ for each program but typically include the origination fee charged by the lender, third party fees including those for appraisal and title insurance and may include mortgage insurance fees if that is a requirement. All of these fees almost always are included in the mortgage, to avoid cash outlays.

Income Taxes: Whether income taxes are due on the amount received from a reverse mortgage depends on the country’s tax code. Since the funds received are loans to the borrower, and loans are not taxable in most countries, funds received through reverse mortgages are mostly not taxable.

Key Case to Watch

THE US REVERSE MORTGAGE PROGRAM

HOME EQUITY CONVERSION MORTGAGE (HECM)

The US Home Equity Conversion Mortgage is an interesting case to follow. A US HECM reverse mortgage enables home owners of 62 or older to borrow against the equity in their homes, with no obligation to repay so long as they live in the home, with multiple options for drawing funds, and with payments guaranteed by the Federal Housing Administration (FHA).

It has seen a disappointing uptake in the past and has been revised recently to address misuse. It holds interesting lessons for other countries interested in implementing a reverse mortgage program.

Here are additional details:

Eligibility: Borrowers must be 62 or older, they must own and occupy the mortgaged house as their permanent residence, and the house must be single family, or in a 2-to4 family structure, in an FHA-approved condominium or an approved manufactured home. Any existing mortgage on the home must be paid off when you obtain the HECM.

Cash Withdrawal Options: One of the valuable features of the US HECM reverse mortgage is that it offers multiple options for drawing funds, which can be used singly or in combination to meet a wide variety of senior needs. The senior may 1) draw cash at closing, 2) retain an unused credit line that grows over time and can be drawn on at the senior’s discretion, 3) receive a monthly “tenure” annuity for as long as they live in the house, 4) receive a term annuity for a period specified by the senior, or 5) combine several of these options.

Mortgage Types: HECMs may be fixed-rate or adjustable rate, but fixed rate HECMs are available only for cash withdrawals. Both fixed and adjustable-rate HECMs come in standard and saver variants, with the saver carrying a lower insurance premium but offering smaller cash draws.

Upfront costs: The origination fee HECM borrowers pay lenders is capped by law at $2500 on house values of $125,000 or less, at $4,000 on house values of $200,000 or less, and at $6,000 on values of $400,000 or more. Some HECM lenders charge less than these maximums. While third party fees vary from one part of the country to another, there are no significant differences between HECMs and standard mortgages.

Mortgage Insurance Requirements: The upfront mortgage insurance premium is .5 percent of property value when the borrower draws no more than 60 percent of his total HECM borrowing power at closing or anytime within the first year. If the draws exceed 60 percent, the insurance premium is 2.5 percent. Since the maximum allowable draw is only 70 percent, borrowers should avoid exceeding the 60percent limit if at all possible. The 60-70 percent rule was introduced in September 2013 as part of a package of reforms designed to reduce losses to FHA, which were exceptionally high in cases where borrowers withdrew the maximum cash allowed at closing.

Some upfront draws are mandated by HUD, including draws used to pay off an existing mortgage loan balance, and to make important repairs to the house. If mandated draws exceed the 60 percent level, the borrower cannot avoid the 2.5 percent insurance premium. The upfront premium is financed. Borrowers also pay a monthly premium on all HECMs equal to 1.25%/12, which is an add-on to the interest due. The premiums compensate FHA for the HECM risks it assumes.

Risk Borne by FHA: FHA assumes two major reverse mortgage risks. One is that the lender obligated to make payments to the senior is unable to do so for any reason. The second is that the property value at time of termination does not cover the outstanding debt.

Equity in the Property: The debt that grows with a HECM must be paid when the borrower dies, moves out permanently, or elects to pay it off voluntarily. Any equity remaining belongs to the borrower or the borrower’s estate. If the debt exceeds the property value, FHA bears the loss, not the borrower or the borrower’s estate.

Borrowers’ Obligations: They must live in the house so long as the HECM remains in force, they must pay their property taxes and homeowners insurance, and they must maintain the property. These are obligations a homeowner has whether they take a HECM or not.

Risk Borne by the Borrower and Co-Residents: The borrower who fails to pay property taxes or homeowners insurance is in default and could lose the house to foreclosure. If the borrower shares the house with another person who is not a party to the HECM contract, such as a young spouse not eligible for a HECM, that person will be obliged to leave the house on the borrower’s death. If there are family members who want to keep the house after the borrower’s death, they must pay off the HECM balance even if it exceeds the property value.

HECM Saver Option: Until November 2013 HECMs offered a Saver version designed for borrowers with short time horizons who wanted to minimize the loss of equity in their home. The initial mortgage insurance premium on a Saver was reduced from 2 percent of home value to 0.1 percent, while the maximum amount that could be drawn was reduced by 15-20 percent, depending on the borrower’s age. The Saver was a useful option for owners who intend to sell their home in a year or two and pay off the HECM with the proceeds.

Why the Recent Changes in the HECM program: FHA made sweeping changes to the HECM reverse mortgage program in November 2013 in response to increasing losses it incurred on the program related to its misuse. A disproportionate number of borrowers were drawing as much cash upfront as they could – 100 percent of the principle limit (PL), which is what FHA calls the senior’s total borrowing power. This left them no scope for further draws in the future. The Saver Program to Discourage Cash Draws Was Unsuccessful and has been terminated. FHA had tried to encourage seniors to take a longer view by creating the saver program as an alternative to the standard program. The saver program offered a sharp reduction in the upfront mortgage insurance program to seniors willing to accept a smaller PL.

The combination of reduced upfront charges and smaller draws resulted in slower growth of future debt on saver HECMs. But the prospect of slower debt growth proved no match for the appeal of cash-in-hand, and the saver program never attracted many seniors.

Under the new rules, borrowers can no longer draw 100 percent of the PL unless the draws are used to comply with FHA mandates. Mandatory draws include paying off all liens on the property including the senior’s existing mortgage if there is one, all settlement costs, and any repairs needed to meet FHA property requirements. Cash draws within the first year for other than mandated purposes (I call these “pocket draws”) are limited to 60 percent of the PL less mandatory draws, or to 10 percent of the PL, whichever is greater. The dual mortgage insurance premium feature has been retained, but now it is based on whether or not total cash draws in the first year are above or below 60 percent of the PL.

See link to the HECM calculator.

Related Documents

| Publish Date | Title | Author | |

|---|---|---|---|

| 2014 | How Do HECM Reverse Mortgages Work? | Jack Guttentag | |

| 2014 | Which HECM Options Best Meet Your Needs? | Jack Guttentag | |

| 2014 | Reverse Mortgage Pricing and Risk Analysis Allowing for Idiosyncratic House Price Risk and Longevity Risk | Adam Wenqiang Shao | |

| 2012 | The Consumer Financial Protection Bureau's Study on Reverse Mortgages | Consumer Financial Protection Bureau |